Notifications

12 minutes, 27 seconds

-207 Views 0 Comments 0 Likes 0 Reviews

The global spinal implants and surgery devices market was valued at USD 11.68 billion in 2023 and is expected to witness substantial growth, reaching an estimated value of USD 18.5 billion by 2032, growing at a CAGR of 4% during the forecast period from 2024 to 2032. This growth is primarily driven by the rising prevalence of spinal disorders, increased awareness of advanced surgical techniques, and an expanding global geriatric population, among other factors.

In this blog post, we will explore the key dynamics of the spinal implants and surgery devices market, including market share, size, trends, growth drivers, challenges, outlook, and segments. Additionally, we will analyse the impact of the COVID-19 pandemic on the market and provide a detailed forecast for the upcoming years.

Spinal implants and surgery devices are used to treat various spinal conditions, such as degenerative disc diseases, spinal deformities, traumatic spinal injuries, and scoliosis. These devices help in stabilizing the spine, promoting healing, and restoring normal functionality. The market has evolved significantly with advancements in implant technologies, surgical techniques, and post-surgical care.

The global market for spinal implants and surgery devices is expanding due to factors like the increasing incidence of spinal diseases, growing demand for minimally invasive surgeries, and the rise of ageing populations prone to age-related spinal conditions. Moreover, the demand for enhanced surgical outcomes and recovery times has accelerated the adoption of advanced spinal implant systems.

The spinal implants and surgery devices market was valued at USD 11.68 billion in 2023, and it is expected to grow at a CAGR of 4% between 2024 and 2032. By the end of the forecast period, the market size is anticipated to reach approximately USD 18.5 billion.

Factors such as technological advancements, rising healthcare expenditures, and an increased focus on improving the quality of life for patients will continue to drive this growth.

Get a Free Sample Report with Table of Contents: https://www.expertmarketresearch.com/reports/spinal-implants-and-surgery-devices-market/requestsample

The rising prevalence of spinal disorders, such as degenerative disc diseases, scoliosis, and spinal stenosis, is one of the primary drivers for the growth of the spinal implants and surgery devices market. Conditions like low back pain, caused by herniated discs or degenerative diseases, have become common across various age groups, particularly as the global population ages.

In particular, the elderly population is more susceptible to spinal injuries and disorders due to weakened bone structures and the natural degeneration of spinal components over time. According to the World Health Organization (WHO), approximately 80% of individuals will experience back pain at some point in their lives, thus increasing the demand for spinal implants and surgery devices.

The shift toward minimally invasive spine surgeries has significantly impacted the spinal implants market. These procedures offer several advantages, such as smaller incisions, reduced recovery times, and lower complication rates. The growing preference for minimally invasive techniques has encouraged manufacturers to develop advanced spinal implants and surgical instruments that facilitate such procedures.

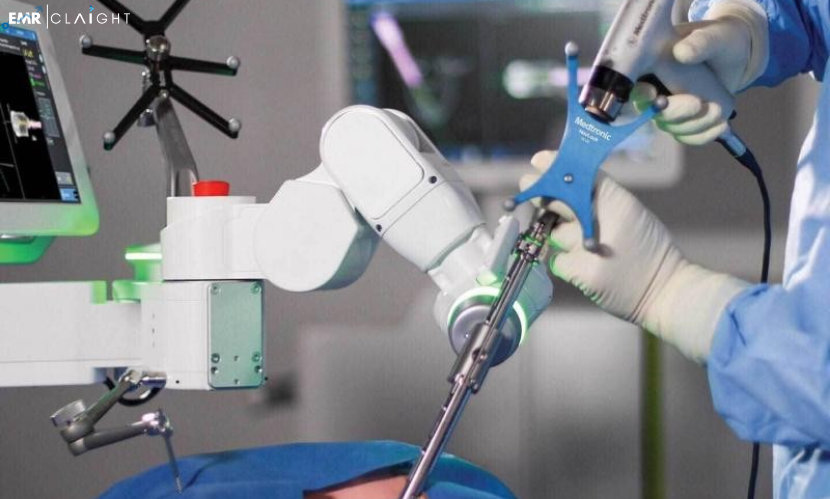

As a result, patients can now experience quicker recovery times and less pain post-surgery, which makes spinal surgeries more appealing. This trend is further enhanced by technological innovations like robotic-assisted surgeries and 3D-printed spinal implants, which have contributed to improving the precision and efficacy of surgeries.

Ongoing advancements in spinal implant technologies, such as 3D printing and robotic surgery, have expanded the scope for the growth of the market. 3D printing allows for custom implants, ensuring a better fit and more personalized treatment plans for patients. Furthermore, the integration of robotic assistance in spinal surgery enhances surgical accuracy, reducing human error and improving patient outcomes.

The increasing adoption of biocompatible materials and smart spinal implants is expected to further drive the market. These implants are designed to interact with biological tissues, enhancing healing and reducing rejection rates, thus increasing the effectiveness of spinal surgeries.

The global spinal implants and surgery devices market is segmented based on product types, applications, and geographical regions. Each of these segments plays a crucial role in shaping the market's growth and development.

The market can be segmented into the following categories:

Spinal Fusion Devices: These devices, including spinal rods, plates, and screws, are primarily used in spinal fusion surgeries to stabilize the spine and promote healing. They dominate the market due to the high prevalence of degenerative spine diseases.

Spinal Biologics: This segment includes bone grafts and bone morphogenetic proteins that help promote the regeneration of bone tissue after spinal surgeries. With advancements in biological materials, this segment is growing rapidly.

Non-fusion Devices: These devices, including artificial discs and motion-preserving implants, are increasingly popular due to their potential to maintain spinal motion and reduce long-term complications associated with fusion surgeries.

Vertebral Compression Fracture Devices: These devices are used to treat fractures of the vertebral body, typically through procedures like vertebroplasty and kyphoplasty. The demand for these devices is expected to grow as the geriatric population rises.

Spinal Surgery Instruments: This category includes instruments used during spinal surgeries, such as surgical tools, drills, and instruments for implant placement.

Degenerative Disc Diseases: The most common spinal disorder treated with implants and devices, degenerative disc disease leads to pain and discomfort. These conditions often require spinal fusion or disc replacement.

Spinal Deformities: This includes conditions like scoliosis and kyphosis, where the spine is abnormally curved. Surgical correction of these deformities often requires the use of advanced spinal implants.

Spinal Trauma: Traumatic injuries to the spine, such as fractures and dislocations, often result in the need for stabilisation implants.

Spinal Tumours: The presence of spinal tumours can necessitate the use of spinal implants to support the spine during tumour removal procedures.

The market can be divided into regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Each region presents unique opportunities and challenges for growth.

North America holds the largest share of the spinal implants market, driven by the high adoption of advanced surgical technologies, a robust healthcare infrastructure, and a growing ageing population.

Europe is expected to witness steady growth due to increasing healthcare expenditures and the growing incidence of spinal diseases.

Asia-Pacific is anticipated to experience the fastest growth in the coming years, largely due to the rising healthcare demand in emerging economies like China and India.

Latin America and Middle East & Africa are expected to see moderate growth, driven by increased healthcare access and awareness in these regions.

As the global population ages, the incidence of age-related spinal diseases such as osteoporosis, degenerative disc disease, and spinal stenosis is increasing. This has resulted in a growing demand for spinal surgeries and implants to restore mobility and alleviate pain.

Governments and private players are investing heavily in the healthcare sector to meet the increasing demand for advanced medical procedures. This is positively impacting the growth of the spinal implants and surgery devices market, especially in regions with high healthcare spending, like North America and Europe.

Technological innovations, including the integration of artificial intelligence (AI), robotic-assisted surgery, and 3D printing, have significantly improved the precision and success rates of spinal surgeries. These advancements are making complex procedures less invasive, improving recovery times, and reducing risks, thereby increasing their adoption.

The COVID-19 pandemic had a significant impact on the spinal implants and surgery devices market. During the peak of the pandemic, elective surgeries, including spinal surgeries, were delayed or cancelled in many regions, leading to a temporary slowdown in market growth. Hospitals and surgical centres focused on managing COVID-19 cases, which resulted in fewer elective surgeries being performed.

However, as the pandemic subsided and healthcare systems adapted to new safety measures, the market rebounded. Post-pandemic, there has been a surge in demand for spinal surgeries due to the backlog of untreated spinal conditions during the pandemic. Furthermore, the rise in telemedicine and virtual consultations has played a role in the increased diagnosis and treatment of spinal conditions, which further supports the recovery and growth of the market.

The outlook for the spinal implants and surgery devices market remains positive, with continuous technological innovations, growing demand for minimally invasive surgeries, and the rising prevalence of spinal disorders all contributing to market growth.

The market is expected to continue expanding at a CAGR of 4% from 2024 to 2032, with the market value projected to reach USD 18.5 billion by 2032. Emerging economies, especially in the Asia-Pacific region, present significant growth opportunities for market players as healthcare access improves and the demand for advanced spinal care increases.

Key market players such as Medtronic, Johnson & Johnson, Stryker Corporation, and Zimmer Biomet continue to innovate and expand their product portfolios, positioning themselves to capitalize on the growing demand for spinal implants and surgery devices.

With increasing technological advancements, rising healthcare investments, and the growing prevalence of spinal conditions, the market is poised for steady growth in the coming years.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}